Root Insurance🚗- stock analysis by Fintech Wave

Hi, ya’all, it’s time for an insurtech stock analysis. This is the first time we are doing a deep dive into insurtech stock. The company is called Root Insurance and its main product is car insurance.

The company is using the mobile app to track driving habits and adjust insurance rates based on that. Pretty innovative concept compared to traditional car insurance companies, but with the current decline in the market, ROOT stock lost 90% of its value in one year. From more than $100 per stock down to $8. We will analyze Root’s business model and financials to check if is it a good stock to invest in. Let’s go👇

Ticker: $ ROOT

Website: joinroot.com

IPO Date: October 28, 2020

Price at IPO: $27 per share

52 Week High: $116

52 Week Low: $7.75

Market Cap: $110M

HQ: Columbus, Ohio

Employees: 1600

Introduction

Root Insurance is founded in 2015 in Columbus, Ohio by Alex Timm (CEO) and Dan Manges. It was the first insurance that adjusts insurance premiums based on drivers’ driving scores which are monitored via a mobile app. This way, they can personalize insurance premiums for each customer. This idea is probably old as the insurance industry, but with technological advances, Root was able to bring it to the real world.

The company became well-known in 2017 after it began offering a discount to Tesla owners who drive using Autopilot mode, making Root the first insurance company to adjust premiums based on the deciding fact of whether the vehicle being insured is operating under semi-autonomous vehicle conditions.

At some point, the company was valued at $3.65B after Series E funding by Coatue. Unfortunately for them, Root became one of the companies that are worth less than the money they raised. In total, Root raises $532M, while the current market cap is only $117M.

On August 11, 2021, Root announced a partnership deal with Carvana (an online car seller) to develop personalized auto insurance programs for Carvana’s online car-buying platform. The deal includes a $126 million investment from Carvana with a 5% stake in Root. The plan in the collaboration is to use both companies' technology to develop an embedded experience for customers at the point of purchasing a car through Carvana.

Apart from car insurance which is Root’s main business, the company also entered into homeowners insurance and renters insurance.

Business model and market

The car insurance market size in the USA is around $320B. Although the industry is huge, there is also a lot of competition - There are more than 500 car insurance providers in the U.S and it is a hard fight for the customers. Basically, every year customers shop for the cheapest insurance around and they will just go where, so it is a nonstop race to cut costs.

As we already learned, Root is tracking customers’ driving to create personalized insurance quotes. Drivers usually need to drive for 12 days after which results are analyzed by artificial intelligence (AI). AI then decides if the driver is able to receive personalized insurance quotes.

Since Root is monitoring customers’ driving habits there are privacy concerns. Every customer needs to think for himself - am I ok to be tracked in order to get cheaper insurance? Personally, I would never agree to an insurance app to track my driving even if they can cut the insurance premium cost by half. Having all these customer data could be a pretty huge reputational risk in case of a data breach.

Also, for most car insurance, you get quotes for 1 year. With Root, you get a 6 month insurance policy, and after 6 months price could go up based on your driving. It’s a good way for Root to be able to increase the price, but I don’t think customers like that.

So far, The Root app has around 11 million app downloads and has collected 18 billion miles of driving data to inform their insurance offerings.

Root Insurance is available in 36 States. We know it’s not easy to get acquire licenses for all states, but it is strange how they are still not licensed to sell insurance in the 18 states. After IPO, they had enough money to get all these licenses.

Apart from car insurance, Root entered into homeowners and renters insurance. It is a good move because they can just upsell these types of insurance to their existing customers.

The property insurance industry is much bigger than car insurance - more than $800B, but the competition is much larger - more than 2500 insurers. There is an opportunity in renters insurance for them - only 45% of renters have insurance, so there is a big undercovered market there.

How does Root make money?

Like every other insurance company, Root is making money from selling insurance policies to its customers. For the insurance business to be profitable the value of insurance premiums must exceed compensation payouts.

Based on data from Insurify.com, the average insurance policy from Root insurance cost $89 if you have a clean driving record. The national average is $77. The company ended Q2 with 297,716 auto policies in force (a decrease of 76,005 compared to Q2 2021).

Premium per auto policy was $1,077, an 11% increase compared to the same quarter of last year. Root doesn’t have any physical branch, which helps keep the costs low.

Their renter's insurance ends up with 7,778 policies with an average $140 premium per policy. They didn’t post the numbers for homeowner insurance.

Apart from insurance premiums, Root also makes money from investments (fee % in total income) - the company is likely investing a small portion of each insurance premium it collects into bonds and stocks.

Financials

As Root also mentions in its Shareholder letter, the last 12 months were very difficult for car insurers - from the pandemic to inflation - a lot of people working remotely canceling car policies. The company did some proactive steps like cutting marketing costs by 77% compared to the same quarter in the previous year.

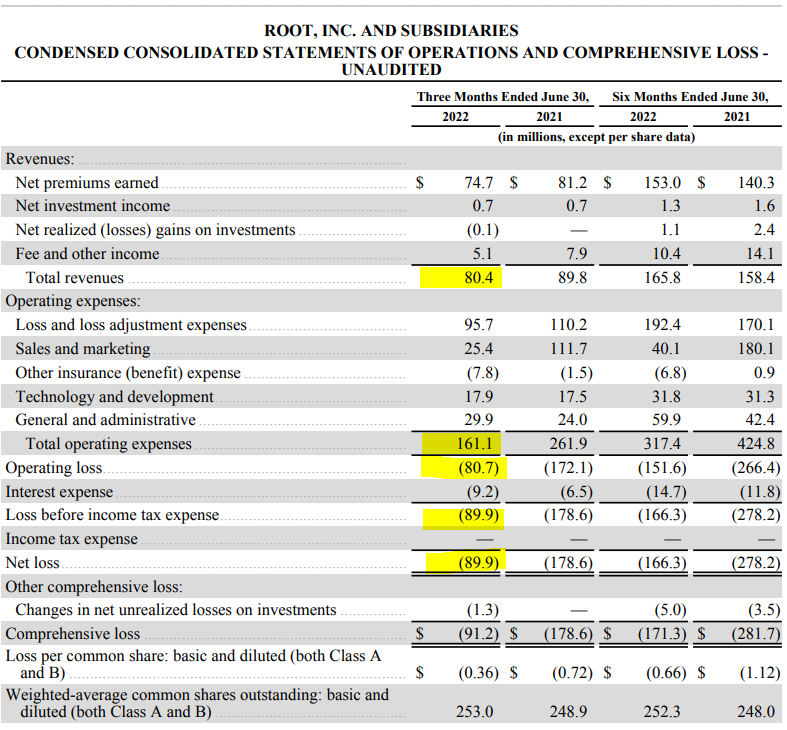

Root has yearly revenue of around $350M. The total revenue for Q2 2022 was $80.4M, while the total operating expenses were $161.1M net loss was $89.8. Although it doesn’t look good for Root, the positive thing is the trend. The loss is much smaller compared to the previous year (Q2 2021 the company reported a net loss of $178.6 million).

Partnership with Carvana is getting momentum - new premium volume from Carvana grew to 31% of new business in Q2’22, which is significant growth from 13% of Root’s new premium volume in Q1 2022. The partnership is paying off for both companies.

Stock History

In one year the stock lost 90% of its value. Part of that is just a bear market (every stock is down), but Root’s stock started losing value before the market correction because investors are questioning if the company can become profitable. They are improving financially every quarter, but it would still take time to get close to profitability.

Conclusion

Personally, we would never use Root Insurance, because we don’t want them to monitor our driving habits. Also, they can increase our insurance premium after only 6 months. Because we don’t believe in this business model we wouldn’t invest in this company, but the technology behind is good so I wouldn’t be surprised if Root would be acquired by a larger insurer. With a current market cap of only $110M and more than 300.000 car insurance policies Root is a valuable target for acquisition. It would even make sense for Carvana to acquire it.