💳Payments for dummies - part 3

Cash and crypto in 10 min read

Aaaaannndd finally, part 3 of our Payments for dummies series is here! Sorry for the long wait, we are focused a lot on subscriber growth at the moment, but we are preparing for you a lot of interesting content, so stay tuned.

For those who didn’t read the first two parts the links are bellow 👇

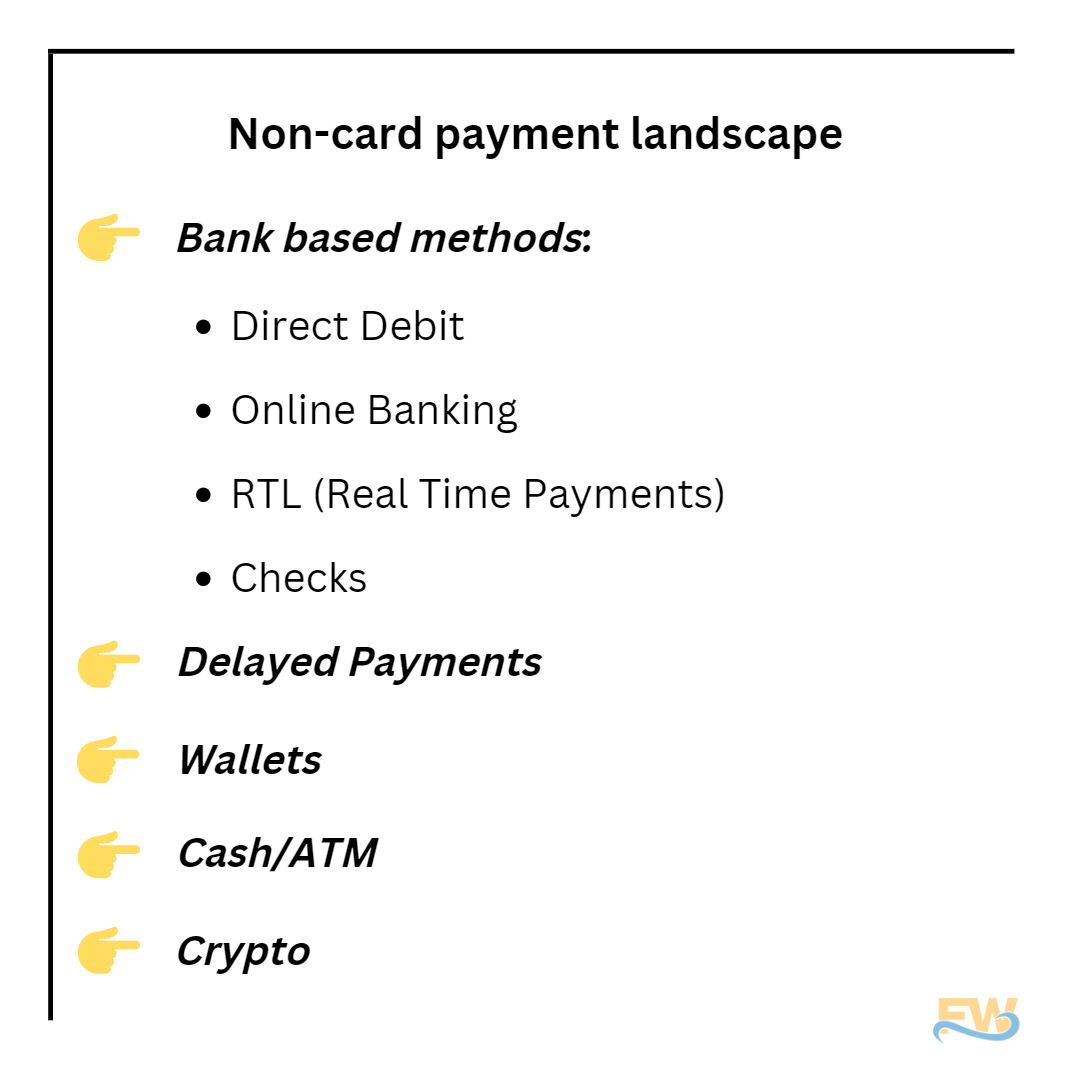

In part 1 we talked only about card payments, and in part 2 we covered non-card payments. However, there are a lot of non-card payment types so we weren’t able to cover them all. Today we will cover Cash/ATM payments and Crypto payments.

Just to freshen up your memory, non-card payments are the following 👇

In case you are not subscribed yet, you can do it here 👇

Also, if you like this post, please share it, it can help us a lot🙏

But, before we start, we have a sponsor today! As always, we are trying to cooperate with cool companies, and today is no exception (in our opinion). Do you know that feeling when you are wearing sunglasses, but depending on the hour, sometimes your sunglasses are too dark, and sometimes to light? Dusk has a solutions for it.

Sponsored content

Meet Dusk, the sunglasses for all seasons

Dusk are the first and only pair of app-enabled smart sunglasses with electrochromic lenses, giving you the power to change the tint level to your exact preference. Check out the five reasons why tens of thousands of people are ditching their regular sunglasses for Dusk...

Our Biggest Sale of the year starts NOW! Get $100 OFF these tint-adjustable audio sunglasses until we sell out!

This is the lowest price we have EVER offered...

WARNING: These smart sunglasses have sold out 4x this year. Order now before it's too late!

Cash/ATM transaction

You must be thinking now “we all know what cash payments are, why do you even write about it”. That might be true, but do you know that cash payment is beeing used as a form of online payment?

In that regard, Cash-on-delivery (COD) is common form of cash payment in the online world. Essentialy, it’s a cash-based payment method that allow someone to pay cash on delivery or take cash to a specified location (conveniance store, ATM etc) to complete online order.

Did you know?

Cash-on-delivery (COD) methods accounted for 3.3% of online transactions globally in 2020, according to a Worldpay report. In the Middle East and Africa, COD was the second leading payment method in 2020. For example, in Nigeria COD accounts for 23,2% of all transactions.

In Latin America and Japan COD is also very popular. Data for 2020 shows that 5,4% of e-commerce spending in Latin America used cash to complete a sale. In Japan, paying with cash at a convenience store, called Konbini, accounted for 10,7% of online shopping.

From a merchant-acceptance perspective, there are key considerations that exist when accepting cash methods. The first is the delay, which occurs on two fronts. First there’s the delay when the transaction is completed by a customer, and they go to pay the amount agreed on. Then there’s the delay in the time it takes for the system to settle a merchant. This is an important consideration for retail merchants who will be shipping physical goods. It’s best practice to wait until the payment method confirms that the customer has paid the balance in full, thus completing the transaction.

Another consideration for merchants is that refunds are not usually supported with cash transactions. This leaves merchants having to build workarounds like store credit, gift cards, or a transfer to the customer directly.

Example

We’ve mentioned before that cash payment in online transactions is quite popular in Brazil, and Boleto is the most popular one.

How does it work?

The shopper selects to pay with Boleto at the merchant checkout online, and a voucher is generated. This voucher can be printed, and the shopper can take it to the bank, ATM, or authorized shop that accepts Boleto payments. The customer can then use cash to complete the Boleto payments. Additionally, Boletos can be paid online by the shopper using online banking via their app.

There are two key things to consider with Boleto payments; expiry and settlement.

Expiry

Merchants can choose how long Boleto voucher is valid; the norm is five days. For merchants selling physical goods, the time of expiry is a very important consideration, because those goods will need to be held until the Boleto is completed or expired.

Settlement

Once the shopper has completed the payment the merchant receives funds in 2 to 3 days. This is a key reason why merchants are keen to offer Boletos - the settlement delay for card payments in Brazil is 30 days. Additionally, Boletos are a fixed fee transaction so they are economical in that regard. Another reason is that 1/3 of Brazil population is unbanked, so a huge portion of the Brazilian population is empowered to make online purchases thanks to Boleto.

Boleto and Brazil are not the only examples of cash payments for online transactions; Konbini in Japan and Oxxo in Mexico are Boleto counterparts.

Crypto payment

Now comes the part that you’ve all been waiting for 😂, Crypto payment. There are many aspects of crypto, but since this is “Payments for dummies” series it would be wise to stick to the crypto part that covers payments, and that would be the core concepts of crypto and DeFI (decentralized finance).

Where does the crypto story start?

With Bitcoin, of course!

Bitcoin beginner level

The Bitcoin White Paper was published on October 28th, 2008 by Satoshi Nakomoto (we don’t know if this is one person or a group). It proposed a novel approach to eliminate the need for middlemen in digital transactions. Bitcoin enabled peer-to-peer transactions online that could inherently be trusted. The transactions are all recorded on an immutable and cryptographically encrypted open ledger called the blockchain.

If you have to compare blockchain with standard terminology in payments, the most accurate comparison is Network in online card payments. In case you don’t know what Network is, please read part 1 of “Payments for Dummies” series.

The trust is built into the code, rather than a middleman like a card network (Visa, MasterCard), so blockchain transactions are often referred to as “trustless”. Majority of people know already that new bitcoins are created by mining, while fiat currencies ($, EUR etc) are created by a centralized authority such as country’s Central Bank.

Now comes the important part of the whole crypto fluff, so pay attention! 💤💤💤

Bitcoin is considered a protocol. What does that mean? In short, it’s the set of rules for how each participant in a blockchain (node) should share data, process messages, and accept processed messages by other participants. Different protocols use different consensus mechanisms to validate a transaction, record them, and generate new tokens. Bitcoin uses a proof of work consensus mechanism, while some other blockchains use proof of stake (proof of stake does not involve mining).

Protocols essentially enable trustless transactions between parties. The community in the protocol verifies and records transactions based on the standards and rules defined by the protocol.

To put everything in simple terms, when you are paying online with a card, the Network sets the rules because there has to be rules (all explained in part 1). But the Network is owned by a company/organization, while with crypto payments…who owns the blockchain? Nobody, and everybody. That is why crypto enthusiasts are so hyped, finally there is a decentralized form of payment, free from any government etc.

“Above” Bitcoin

Now that you know what bitcoin is in a nutshell, it’s time to introduce a new term, the Lightning Network (LN). LN is also known as a “layer 2” payment protocol - it’s layered on top of existing cryptocurrency protocols. The LN was designed to support fast transactions at a lower cost than a typical bitcoin transaction and increasing scalability by supporting upwards of 65,000 TPS (transactions per second). It aims to solve the problem with a standard bitcoin blockchain transaction - speed and cost. A typical bitcoin transaction can take an hour (10 TPS), and given its high fees, it can render small transaction size impractical.

Ethereum

While we are at “layer 2” payment protocol, it would be rude not to mention Ethereum, the second largest crypto in the world. The idea of Ethereum as a blockchain is to support wider use cases than just P2P (person to person) payments and to increase functionality. Ethereum today is an ecosystem of dApps, tokes, and other “layer 2” protocols. Ether (ETH) is the native cryptocurrency that fuels the network and is used to pay transaction fees.

The largest difference between Bitcoin and Ethereum is that Ethereum is built to support more use cases than P2P transactions. Today there are over 3.000 dApps (decentralized applications) on Ethereum, which has made the protocol synonymous with DeFi.

DeFi

If we ask Wikipedia, DeFi offers financial instruments without relying on intermediaries such as brokerages, exchanges, or banks by using smart contracts on a blockchain. DeFi is just an “umbrella” term for everything that is considered decentralized finance, but the real star is the term smart contracts.

Smart contracts are, simply put, code that defines cause and effect. When the first part of the contract is completed, a secondary action follows. They facilitate, verify, and enforce an exchange with agreed-upon rules allowing for a complex ecosystem of trustless decentralized interactions. With smart contracts no third party is needed to finalize the actions. No more waiting, no more middleman…

Did I say middleman? Let’s go back to card payments in the online world. Just to recap (part 1 of the series, again), all the parties needed to make a card payment (merchant, merchant acquirer, cardholder, issuing bank) are connected through the Networks. These Networks are the centralizing function; they make the rules, lay out many of the correlated fees and costs of payments, and act as a conduit of data and funds.

DeFI takes away the need for centralized control; rather than a private company (though many Networks are publicly traded companies), transactions are enabled and guaranteed by smart contracts.

To go even further out of the centralized world, DeFi and crypto in general enable users self-custody. An individual can be their own bank, and securely hold tokens and transact with them.

So basically, if you want to, with crypto and DeFi you can potentially be 100% “off the grid” in terms of governments, other companies etc. But, is it really “free”?

Fees

Hm, no middleman, decentralized…there are no networks and issuers that are taking their cut from transactions? Pleaseee, where do I sign?

While there is no individual entity setting the rules of engagement and related fees, fees do exist. For instance, in the Ethereum network, fees are called “gas” - the amount of ETH that’s paid to a node to process the transaction. Gas is paid by the user initiating a transaction to the miner who validates the transactions; this then incentivizes nodes to maintain the network.

Btw, maybe you will sometimes encounter the term “gwei”. Gas fees on Ethereum are denominated in a unit called “gwei” which is equal to 0.000000001 ETH.

Fees are used to perform a transaction and document it across nodes on the blockchain. In today’s world, gas fees can be high enough that they make interchange fees look cheap (again, I’m referring to part 1 of this series).

More complex transactions require more gas, such as DeFi transactions on smart contracts. To solve this high gas problem many projects are working on new solutions but still, nothing came out yet that is universally accepted.

How crypto transactions work - for beginners

We’ll keep it simple here. A wallet is used to store private keys, which prove ownership of your assets so it’s important to never share your private key with anyone. You can generate public keys that can be shared without risking the security of your assets.

Above mentioned wallet can be a software, a piece of hardware for self-custody, or it can be kept on an exchange if they have custody of your funds. Think of this way; trusting an exchange with your private keys is similar to how you trust a bank with holding your cash.

So how does it all work? Let’s start with receiving crypto.

To initiate a transaction, you share your public key, or sometimes a shortened version called an address. Anyone can send a transaction to your public key, and then you use your private key to “unlock” the assets. Transactions then must be signed using your private key to validate that you own the public key. This completes the transaction and proves you’re now the owner of those funds.

Crypto transactions are always push transactions and irreversible: you share your public key, and the other party sends you assets. The same goes when you send a user crypto - they provide their public key or affiliated address, and you send funds to them.

In case you do a typo and send by accident money to a different public key…there is no way to return the money.

If we compare crypto and blockchain with other forms of payment, mainly online card payment, there is still a gap. For instance, some aspects of “typical” payments that we take for granted have still not been solved for in crypto. There still needs to be progress in aspects like risk, disputes (like chargeback), and fraud for payments to reach parity with fiat and existing network rails.

But, crypto development is fast, and there is a lot of promise to future solutions and implementations. The hype with crypto started with bitcoin and a lot of people earned and lost money during last 2 years. But, the real value of crypto is not in crypto currencies, it’s in the blockchain and technology behind it. Maybe crypto will never become form of payment, but blockchain will find it’s value, that is for sure.