Payments for dummies - part 2 💳

Hi all,

we are back with another edition on payments for dummies. In the first edition we covered card payments, and today we will cover some of the non-card payment types. Initially, we wanted to make this “Payment for dummies” to be 2 part series, but we will make it 3 part series. It’s just too much information to squeeze into 2 part series. Like the last time, as a reference, we are using the book “The Field Guide to Global Payments” by Sophia Goldberg 👇

Field Guide to Global Payments

In case you haven’t read the first part, here is the link to it 👇

However, before we continue our payments journey, we would like to quickly introduce our sponsor for today! It’s a cool product that we believe you will love👌

Sponsored content

For all of you Apple lovers (me included), there is a cool Indiegogo campaign going on that you should check out 👇

Horizon 3-in-1 MagSafe Wireless Charger

There's a lot to love about Horizon. It charges your Apple devices all at once at the fastest possible speed. It has two flexible, patent-pending hinges, which means it can be used in eight different charging positions. It's compact, portable, and light enough to take anywhere (even though it's also made from aircraft-grade recyclable aluminum). But what we love the most is that Ampere, the brand behind the product, has had several successful crowdfunding campaigns and that tens of thousands of people love their products.

Don’t tell anyone, but Fintech Wave readers get 110$ extra off 😉

*Please note that Horizon's MagSafe panel works with the iPhone 12 onward, and it works with all Apple Watch series.

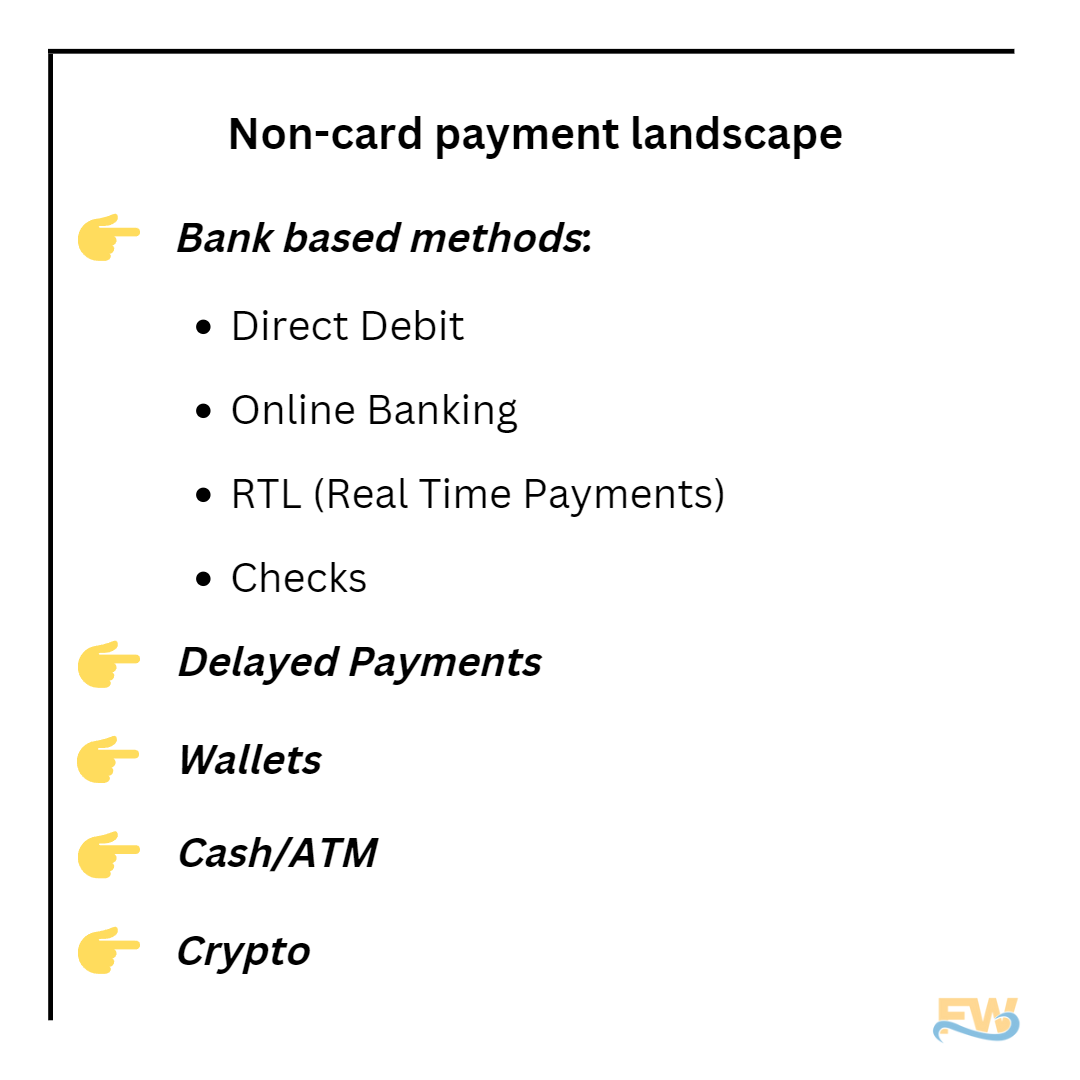

Non-Card payment

If you are like me (Millenial here) you pay most likely everything with your debit/credit card, and even though 💵 is the king, you just hate going to ATM. But, that doesn’t mean that non-card payments are not important. For instance, in China, 21% of online payments are with cards (they pay a lot with wallets), while in Brazil paying for an online transaction with cash is normal. If we look at Europe, in the Netherlands bank transfers via iDeal are the most common way to pay.

Speaking roughly, we can divide non-card payments like this

Bank-based methods

Before we dive into bank-based methods, just explain two important concepts that will help you understand the subject matter. The key governing concept of bank payments is push vs pull. To put it into the perspective; does the customer send funds (push), or do they give the merchant/seller their banking info to let them pull those funds?

Ok, now that we solved this, let’s move on to the first bank-based method!

Direct Debit

A direct debit is “permission to pull". An individual or entity provides a merchant with their banking details and permission to withdraw funds directly from their account under specific terms (monthly subscription, rent payments, utility payments, etc).

Fun fact #1

Direct Debit was created by Unilever in 1964. as a way to collect money from ice cream shops, rather than the existing options of cash, check, or standing order at a bank. Unilever is not, by all means, a financial institution, but its invention in the following 50 years grew in popularity enough to account for 20% of all cashless payments in the EU by 2016.

Two terms are super important when we talk about Direct Debit methods: ACH and SEPA. ACH is used in the USA, and SEPA is used in the EU. If we have to make a connection to part 1 of Payments for Dummies, think of them as Networks in card payments.

ACH & SEPA

ACH stands for “automated clearing house”, and it’s the direct debit rail in the USA. It grew out of check processing in the 1970s, though while checks are a pull method, ACH supports both push and pull. ACH is a bank-owned utility, and NACHA (National Automated Clearing House Association) is responsible for managing regulations and rules. NACHA is a non-profit network of banks that joined together to enable easy movement of funds between the banks using account and routing numbers and a batch process. It is also the body that enforces rules for over 10.000 of the member banks and participants (payment processors, businesses, etc).

Direct debit rail in Europe is called SEPA (Single Euro Payments Area). It works alongside online banking services in individual European countries, like Sofort in Germany and iDeal in the Netherlands. Many European countries prefer bank transfer methods to debit or credit cards, so SEPA is a great way for merchants with recurring models (like Netflix) to support recurring payments. The first transaction will be with a customer’s online bank as a “push” transaction, but the merchant stores the banking details for subsequent direct debit “pull” transactions over SEPA.

If you want to know more 💡

Direct debit is the backbone of B2B payments, and any larger, recurring transactions such as payroll, bill pay, and vendor payments. More than 82% of electronic payments in the USA are processed over ACH. It’s cost-effective when compared to payment methods like credit cards which are expensive for large transaction sizes.

Even though it’s a great option compared to cash or check, in relation to other digital forms of payment, direct debit has a few weaknesses. Payments take a few days to clear/settle. BACS in the UK is typically 5 days, and SEPA in the EU is 3 days. Additionally, it can take a few days before a merchant knows that a payment has failed; the common reason being insufficient funds.

Online banking

Online banking is seemingly straightforward; a shopper initiates the payment from their bank account to a 3rd party like a merchant (the shopper “pushes” the funds). Even though online banking is a simple payment method, there can be hurdles with this payment option, especially in terms of e-commerce. “Push” methods are sometimes also referred to as a “bank redirect” method because a shopper is redirected to their bank portal so they can complete the payment and push funds to the merchant. This can sometimes require multiple web page redirections, or for mobile commerce, an app switch to the relevant banking app, and ideally a switch back to the browser or merchant app then the transaction is complete.

In some countries, such as the Philippines, the online banking rails are open only during normal banking hours (9 am to 5 pm). In Malaysia, online banking is offline between midnight and 1 am for the reconciliation process. Sometimes a bank may be offline in a country and a shopper may wonder why they cannot complete a transaction. The shopper must be present to authenticate the transaction, so there’s no option for the merchant to queue the transaction, like with storing and retrying a card transaction.

RTL (Real-time payments)

We can argue that RTL is a subset of online banking, but it’s distinct enough to have a separate mention. The idea behind RTL is to overcome some of the time inconsistency and settlement delay issues that come with typical online bank payments. Many countries are developing these systems at a national level. They are real-time; always online 24h a day, 7 days a week, 365 days a year; and have messaging as well to confirm the completion of transactions (unlike ACH and checks)

Still, confused about RTL? Why don’t we explain them on two actual RTL initiatives, UPI in India, and PIX in Brazil?

UPI

UPI (United Payments Interface) was created by the NPCI (National Payments Corporation of India), and it’s a great example of open banking. Both UPI and NPCI steam from the Indian government’s “Digital India” initiative which has the goal of digitalizing and pushing for cashless payments across the country, in part to improve the ability to track the flow of money in the economy and reduce tax evasion. NPCI developed UPI as a payment method, and regulators require all merchants that transact more than five hundred million INR (Indian rupee) per year to accept UPI and RuRay payments.

How does it work?

Each user registers a VPA (Virtual Payment Address) with their bank. You can think of this as an alternative to the routing and bank account numbers used in the USA. Rather than being a long string, the VPA can be short and memorable. During the transaction the VPA is used to look up the account holder, a real-time authorization occurs, and the account holder performs authentication over SMS or pushes notification.

The development of UPI and bank infrastructure was the reason why WhatsApp managed to introduce WhatsApp Pay in India. Listen to what Mark Zuckerberg has to say about it 👇

PIX

Pix is one of the newer RTP systems globally; it was launched in November 2020 by the Central Bank of Brazil. By November 2021, 62% of the Brazilian population was registered😦

Like UPI, Pix does away with the need to share bank accounts and routing numbers. For P2P payments (person2person) a user can provide their phone number, their CPF (tax ID number), email address, or a Pix code that is randomly generated. Pix can be also used for consumer and B2B payments.

To pay with Pix, a user can either complete a transaction with a QR code or c/p a code. That user can link whichever bank accounts or wallets (up to 5) they want to use for Pix transactions. Pix offers instant settlement and is online 24h a day/7 days a week/365 days a year. Compared to the 30 days settlement delay for card payments in Brazil, Pix is very merchant and user-friendly. It’s also much cheaper than bank transfers and card fees, which explains the rapid adoption of the system by merchants as well.

Checks

Checks as a form of payment are very USA-focused so we won’t go into too many details there. Although checks feel quite outdated today with all of the digital forms of payment, they were the first interoperable way to pay. You could have a payer with a different bank than the payee’s bank, and a check would allow funds to flow between those two different banks. Another interesting thing about checks is that they have no fees.

The checks did go through the modernization phase (in the USA). In 2004, the Check Clearing for the 21st Century Act - referred to as Check 21- was passed. It gave banks the ability to create digital images of checks, which could then be sent electronically for processing. The main goal of this act was to reduce the cost associated with paper check processing, especially the need to physically transport the checks.

Fun fact #2

At one point in time, the Federal Reserve had a fleet of jets (at times more than 100) to transport checks across the USA daily. In 1995, the Federal Reserve spent over $35 million on the logistics of moving checks alone

Fun fact #3

The Check Clearing for the 21st Century Act was not developed because FED wanted digitalization, it was because of 9/11. For a week after 9/11, all air travel was shut down domestically, which led to a crisis as checks backed up. Check 21 came out of that minor crisis to allow the fully electronic clearing of checks.

Delayed Payments

This is a joined category for installments and open invoices. We will cover BNPL (Buy Now Pay Later) and part of the installments.

Installments

Within the taxonomy, there are two subtypes: one where the merchant is paid as shoppers complete payments (Merchant paid over time), and one where the merchant receives funds up front (BNPL). We know that BNPL is a hot theme at the moment, but we will keep it short here. There will be a separate issue on it in the following weeks.

Fun fact #4

Installments, as we know them today really, got their start in the 1840s for pianos, elegant furniture, and sewing machines. Singer Sewing Machines are credited with driving consumer understanding and interest in installments - their innovative credit plan had the tagline in the 1890s “dollar down, a dollar a week”.

Merchants paid over time

This type of installment payment is popular in Latin and South America. They began as agreements between consumers and individual retailers to make larger purchases possible for low-income consumers and those without formal credit or bank accounts. This type of installment is popular in Brazil and Mexico. In Brazil, the installment is processed by the card networks, and the merchant is settled by the networks as the shopper’s payment is cleared.

Also, installments can be supported by the Issuers. For instance, in Brazil, a merchant doesn’t need to add a separate payment method to offer installments to a shopper. They can specify the number of installments in the authorization request, and the issuing bank manages the installment billing.

The downside of the “Merchant paid over time” is cashflow issues for the merchant. A merchant could theoretically wait a year to be paid in full if they’ve offered 12 months of installments. There is a potential for “advancements” where the acquiring bank settles the merchant before the funds have cleared in the system, charging an interest rate on top for the services. This is very similar to BNPL, with only subtle differences.

The merchant receives funds upfront (BNPL)

For a merchant, this is a better alternative than the previous one because the merchant receives funds upfront and 3rd party provider is responsible for managing all the risks associated with installments payment. From a merchant cash flow perspective, BNLP is similar to cards. However, getting approved for a BNPL purchase can be easier for many shoppers than applying and getting accepted for a credit card.

But, what is the catch with BNPL compared to credit card payments?

Typically higher fees 👀

BNPL providers charge merchants an MDR (merchant discount rate, a blended fee) ranging from 2-6%. Despite the high rate; especially when you consider that BNPL transactions are for more expensive items, and thus a higher % MDR adds up quickly, merchants have been fast to offer BNPL. Why?

Studies and sales teams have shown that consumers spend 55% more when using BNPL.

Open invoice

This way of paying is popular in some European countries. Here a shopper checks out but isn’t charged until 14 to 28 days after their goods are delivered. Open invoices grew out of the catalog era of shopping. Large mail-order companies would let shoppers try something before payment. For instance, in Germany, 90% of merchants offer open invoicing, and some statistics say that 63% of online purchases in Germany are made using this method.

I’m not from Germany, but maybe someone from there can give us their personal view on this?

Actually, Klarna, the Swedish fintech giant, began as an open invoice payment method. They helped encourage online shopping by supporting this low-risk “try before you buy” behavior for e-com.

Wallets

Wallets are a very interesting form of payment and they deserve our attention given their increased adoption. But, as with everything we first need to understand basic taxonomy. With wallets, there is one key question: does the wallet hold a user’s funds?

The first question is if the operator of the wallet holds funds. If the answer is yes, it's a staged wallet. In this case, the wallet holder adds funds via a bank account, cash, or card.

If the answer is no, and the wallet holds payment credentials like a card number or bank account details, it’s a pass-through wallet.

There is also one other distinction between wallets, closed or open-loop wallets. An example of a closed wallet would be Starbuck’s balance for in-app pre-ordering of coffee. You can use that wallet only for Starbucks. Open-loop wallets on the other hand are not tied to a single store/brand.

Fun fact #5

Wallets started with Coca-Cola. They’re credited with processing the first mobile wallet payment in 1997. Coca-Cola created a special vending machine in Finland where a customer could pay for their drink over a text message.

Fun fact #6

China is the country with the biggest adoption of wallets; 72,1% of all online transactions in 2020 were with digital wallets. For comparison, the global average in 2020 was 44,5%.

If you have to remember just one thing about wallets, then remember network tokenization. Network tokenization is the real game changer for wallets and the payment industry.

A network token is a 16-digit number that is provisioned or created by the network affiliated with a card. A network token is not the same thing as 16 digit PAN on cards, and a network token is outside of PCI scope.

For instance, we know Apple Pay allows a user to store their card on their iPhone (or wallet, or another iOS device). But this action has one obvious issue: 16-digit PAN (or card number) is a highly secure piece of data with high-security standards for storing it - PCI. Yet, your phone is not a PCI secure environment…so how do we solve security?

The solution that was created was called the DPAN, or device PAN. DPAN is referred to as a network token today. In short, a DPAN can be provisioned when a cardholder wants to add their card to the Apple Pay wallet. The affiliated network, says Visa, returns a DPAN to Apple, which can then store this in the wallet and also use it to initiate transactions. DPAN has a 1:1 relation to a user’s card and can be used to authorize a transaction.

Because the DPAN is outside of PCI scope by design, another security layer was needed. A cryptogram tied to the device that holds the DPAN is created to secure the transactions, and it’s sent alongside the DPAN in transactions. This allows the card’s issuer to know that this DPAN is used properly. If there is a data leak and DPAN is taken off the phone, it’s useless on its own to authorize a transaction. The cryptogram adds the necessary layer of security.

The game changer…

DPAN began to have utility outside of the wallets, most importantly in e-commerce. E-commerce companies love wallet payments because they offer 1 click checkouts which drive conversion rates. But more importantly, they offer them an opportunity to store shopper payment details without dealing with PCI compliance. Network tokens allow a merchant to store payment credentials themselves without the same level of the security risk of ongoing operational and compliance investments.

In short, merchants can now receive updated card details like when the card expires, directly from the networks rather than reaching out to their customers.

There are many wallets available on the market, but here is just a quick overview of some of them

This is it for now on the wallets. There are interesting stories about PayPay, ApplePay, Alipay, WeChat Pay, and many more, but we will cover this in a separate edition. Maybe it will be a part of Payment for dummies part 3, who knows!

But, what we do know for sure, is that in Payment for dummies part 3 we will cover Cash/ATM payments and Crypto payments! Part 3 will come out next week on Thursday, so stay tuned!

Until then, maybe you can share this post to help us reach more people.